Development and trend of industrial robot market in the first half of 2019

Date:2019-11-19

With the rapid economic growth, the pace of industrial structure transformation and upgrading is also accelerating. Industry 4.0's, is the era of using information technology to promote industrial innovation, human labor has been difficult to meet the needs of enterprise development, industrial robots have become the new favorite of the production profession. It not only takes on the task of freeing human beings from heavy and repetitive labor, but also is necessary for the large-scale and precise production of the manufacturing industry, and even solves the problem that human beings are difficult to complete the work under the risk and harsh environment. Now the variety of industrial robots is complex. According to the variety, they are divided into transfer robots, installation robots, welding robots, joint robots, rectangular coordinate robots and so on, which are widely used in all aspects of industrial production.

After collecting and sorting out the relevant data of industrial robots in the first half of 2019, analysts of fast track Research Institute cooperated with users to analyze and comment on the development trend of domestic industrial robot shopping malls.

China is the largest market country of industrial robots

In 2013, the sales volume of industrial robots in China was 36600, surpassing Japan for the first time, becoming the world's largest industrial robot production and marketing country. In 2015, the sales volume of industrial robots in China was 68500, accounting for 27.7% of 247000 in the world, surpassing one quarter of the global total.

In 2013, the sales volume of industrial robots in China was 36600, surpassing Japan for the first time, becoming the world's largest industrial robot production and marketing country. In 2015, the sales volume of industrial robots in China was 68500, accounting for 27.7% of 247000 in the world, surpassing one quarter of the global total.

In 2017, the sales volume of industrial robots in China was 138100, an increase of 58.7% year-on-year, the fastest growing year. By 2018, the sales volume of industrial robots in China has reached 156400, ranking first in the world for five consecutive years.

Development process of industrial robots

From 1940s to 1960s is the beginning of the development of industrial robots. The digital control machine tool developed by MIT in 1952 has a program control system. Compared with the traditional handicraft industry, the advantage of automatic processing equipment is more obvious, more accustomed to the demand of mass production, and gradually replaced the position of human.

From the 1970s to the 1990s, industrial robots developed in the middle period, marked by automatic production lines. In this stage, with the improvement of production power requirements, a more integrated automatic production line is presented. Together with CAD, cam and other virtual software, it is also used in the design and production of engineering. This automatic production line combining hardware and software is more suitable for batch production and processing.

After the 1990s, with the rapid development of computer technology, it is integrated with the industrial industry, and more integrated, more professional, more intelligent industrial robots appear, and continue to develop in a deeper and broader direction. Nowadays, many industrial robots have the ability of walking, perception and strong environment self habit.

Industrial robots account for more than 50% of the four families

Although China is now the largest industrial robot market in the world, the proportion of foreign-funded enterprises is still very high. The four families of FANUC, KUKA, abb and Yaskawa occupy the first proportion of shopping malls. In the first half of 2019, the proportion of shopping malls is 16.5%, 13.4%, 12.9% and 11.7%. Fanaco is a Japanese numerical control company, with 240 robot products, which are widely used in installation, transfer, welding, casting, spraying, palletizing and other production links. It is also the only robot company in the world.

Although China is now the largest industrial robot market in the world, the proportion of foreign-funded enterprises is still very high. The four families of FANUC, KUKA, abb and Yaskawa occupy the first proportion of shopping malls. In the first half of 2019, the proportion of shopping malls is 16.5%, 13.4%, 12.9% and 11.7%. Fanaco is a Japanese numerical control company, with 240 robot products, which are widely used in installation, transfer, welding, casting, spraying, palletizing and other production links. It is also the only robot company in the world.

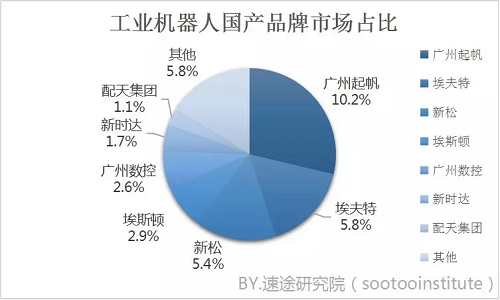

The proportion of domestic industrial robots has increased

Limited by the suppression of foreign enterprises, the market share of domestic brand industrial robots is relatively low, but in recent years, it has made rapid progress and the proportion of shopping malls is expanding. In the first half of 2019, domestic brands accounted for 35.8%, among which Guangzhou sail accounted for 10.2%, which is the largest proportion of domestic robot brands. Guangzhou sail is mainly engaged in the development and production of right angle, joint robot and peripheral supporting equipment, covering spraying, stacking, transfer, machine tool loading and unloading, cutting, welding, polishing, laser and other professions. Secondly, the proportion of leave between Everett and Xinsong is 5.8% and 5.4%. Among them, the fully domestic robot joint is also rising slowly, for example, Shenzhen Tycoon (specializing in R & D and production of robot joint module), accelerating the industrial production of domestic robots.

Limited by the suppression of foreign enterprises, the market share of domestic brand industrial robots is relatively low, but in recent years, it has made rapid progress and the proportion of shopping malls is expanding. In the first half of 2019, domestic brands accounted for 35.8%, among which Guangzhou sail accounted for 10.2%, which is the largest proportion of domestic robot brands. Guangzhou sail is mainly engaged in the development and production of right angle, joint robot and peripheral supporting equipment, covering spraying, stacking, transfer, machine tool loading and unloading, cutting, welding, polishing, laser and other professions. Secondly, the proportion of leave between Everett and Xinsong is 5.8% and 5.4%. Among them, the fully domestic robot joint is also rising slowly, for example, Shenzhen Tycoon (specializing in R & D and production of robot joint module), accelerating the industrial production of domestic robots.

Policy support for robot career development

The rapid development of China's industrial robot market is inseparable from the strong support of the national policy. In May 2015, the "made in China 2025" document mentioned that the bottleneck of key parts and system integration design and production such as robot body, reducer, servo motor, controller, sensor and driver should be broken. In March 2016, the Ministry of industry and information technology, the national development and Reform Commission and the Ministry of Finance jointly issued the development plan of the robot industry (2016-2020). It was mentioned in the document that the annual output of industrial robots with independent brands should be more than 100000, and the annual output of industrial robots with six axes and above should be more than 50000, and more than five robot industrial clusters should be built.

The rapid development of China's industrial robot market is inseparable from the strong support of the national policy. In May 2015, the "made in China 2025" document mentioned that the bottleneck of key parts and system integration design and production such as robot body, reducer, servo motor, controller, sensor and driver should be broken. In March 2016, the Ministry of industry and information technology, the national development and Reform Commission and the Ministry of Finance jointly issued the development plan of the robot industry (2016-2020). It was mentioned in the document that the annual output of industrial robots with independent brands should be more than 100000, and the annual output of industrial robots with six axes and above should be more than 50000, and more than five robot industrial clusters should be built.

Analysts of fast track Research Institute think: as the largest industrial robot market in the world, China is still in the stage of low-end surplus of local brands and lack of supply of high-end products. Foreign brands have long been the leading force. Secondly, in the field of industrial robots, the upstream core parts are still the short board locations of Chinese enterprises. High-end products such as reducers, servo motors, controllers and so on need to be imported. These core parts determine the overall function of the robot, improve the localization level of the core parts, and become the key to the rapid development of industrial robots in China. Of course, in the market with fierce competition, the price has always been the dominant place for domestic brands, which can be relied on in the future

After collecting and sorting out the relevant data of industrial robots in the first half of 2019, analysts of fast track Research Institute cooperated with users to analyze and comment on the development trend of domestic industrial robot shopping malls.

China is the largest market country of industrial robots

In 2017, the sales volume of industrial robots in China was 138100, an increase of 58.7% year-on-year, the fastest growing year. By 2018, the sales volume of industrial robots in China has reached 156400, ranking first in the world for five consecutive years.

Development process of industrial robots

From 1940s to 1960s is the beginning of the development of industrial robots. The digital control machine tool developed by MIT in 1952 has a program control system. Compared with the traditional handicraft industry, the advantage of automatic processing equipment is more obvious, more accustomed to the demand of mass production, and gradually replaced the position of human.

From the 1970s to the 1990s, industrial robots developed in the middle period, marked by automatic production lines. In this stage, with the improvement of production power requirements, a more integrated automatic production line is presented. Together with CAD, cam and other virtual software, it is also used in the design and production of engineering. This automatic production line combining hardware and software is more suitable for batch production and processing.

After the 1990s, with the rapid development of computer technology, it is integrated with the industrial industry, and more integrated, more professional, more intelligent industrial robots appear, and continue to develop in a deeper and broader direction. Nowadays, many industrial robots have the ability of walking, perception and strong environment self habit.

Industrial robots account for more than 50% of the four families

The proportion of domestic industrial robots has increased

Policy support for robot career development

Analysts of fast track Research Institute think: as the largest industrial robot market in the world, China is still in the stage of low-end surplus of local brands and lack of supply of high-end products. Foreign brands have long been the leading force. Secondly, in the field of industrial robots, the upstream core parts are still the short board locations of Chinese enterprises. High-end products such as reducers, servo motors, controllers and so on need to be imported. These core parts determine the overall function of the robot, improve the localization level of the core parts, and become the key to the rapid development of industrial robots in China. Of course, in the market with fierce competition, the price has always been the dominant place for domestic brands, which can be relied on in the future